Important note: If you efiled (or filed) your 2019 Tax Return later in 2020 (after September), then the IRS most likely will NOT have an updated 2019 AGI for you in their systems. Therefore, you will need to enter “0” as your prior-year AGI when you efile your 2020 Tax Return (see instructions below for more details).

Why isn’t my AGI on my tax return?

If your return was rejected for an AGI or PIN mismatch, it means that what you entered doesn’t match their records. The IRS only requires one of these to match their records to get accepted. Double check your prior year AGI and that you entered the correct amount on the Prior Year AGI screen.

Do they look at Agi or taxable income?

AGI: When It Matters In the United States, adjusted gross income is the baseline amount used to determine taxable income, along with a number of other personal finance matters. If you’re using an online tax service to file your income taxes, the service will usually calculate your adjusted gross income for you.

Do banks use AGI or taxable income?

Banks use only your regular gross income to qualify you for a loan. They do not use occasional overtime pay or a potential annual bonus, unless you can convince your loan officer that you will receive one or both of these on a consistent basis in the future.

When does the IRS use your prior year AGI?

Your Prior-Year AGI is the Adjusted Gross Income on last year’s 2019, tax return. The IRS uses your prior-year AGI to verify your identity when you efile your 2020 Tax Return.

Are there limits to how much AGI you can claim on taxes?

Depending on your filing status, you may be subject to an AGI limit—a dollar amount that limits the deductions you can take—which usually applies to higher income earners. Generally, the more deductions and credits you take, the lower your taxable income.

What happens if my AGI is wrong on my 2020 tax return?

An incorrect 2019 AGI on your 2020 return will result in a tax return rejection by the IRS and/or State Tax Agency. It is easy to correct your AGI and resubmit your return if this happens.

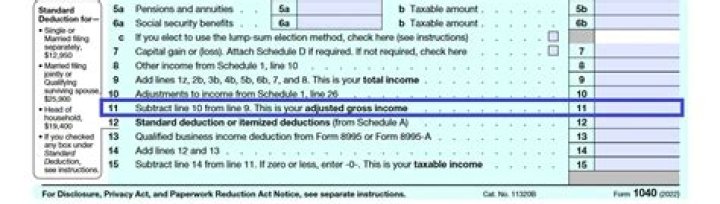

How is the adjusted gross income ( AGI ) calculated?

Determining AGI The IRS defines AGI as “gross income minus adjustments to income.” Depending on the adjustments you’re allowed, your AGI will be equal to or less than the total amount of income or earnings you made for the tax year. Remember to consider all sources of income that contribute to your AGI, including: