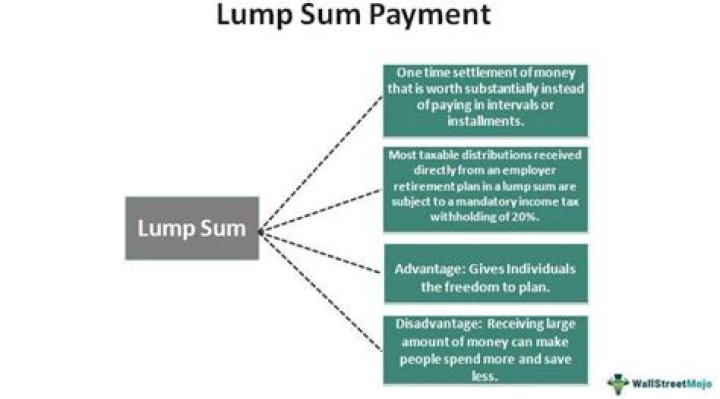

A lump-sum payment is an often large sum that is paid in one single payment instead of broken up into installments. They are sometimes associated with pension plans and other retirement vehicles, such as 401k accounts, where retirees accept a smaller upfront lump-sum payment rather than a larger sum paid out over time.

A lump-sum payment is an often large sum that is paid in one single payment instead of broken up into installments. It is also known as a bullet repayment when dealing with a loan.

How do I report a lump sum payment?

You must include the taxable part of a lump-sum payment of benefits received in the current year (reported to you on Form SSA-1099, Social Security Benefit Statement) in your current year’s income, even if the payment includes benefits for an earlier year.

What are the disadvantages of taking a lump sum payment?

The main disadvantages to taking a lump sum payment over a salary continuance are: • The lump sum package is usually discounted more than a severance package based on a salary continuance model since mitigation and or set off for new employment income is factored into the employer’s reduced offer; and.

Can you take a lump sum pension buyout?

A pension buyout offer is not readily available for most employees and thus it is a scenario that many have never even contemplated. Below are fictitious numbers, but they are presented in relative proportion to how the pension buyout offer from GE was presented to me in my offer letter. Option A: Take a one-time lump sum in the amount of $150,000.

How does a lump sum relocation package work?

Lump sum relocation packages allow employees to prioritize needs and expenses according to the money available to them in the package. This can make it easier for businesses to control the costs and reduce the record-keeping and expense tracking burden on the employer.

Is it better to take a lump sum or a cash out?

A lump-sum payment may seem attractive. You give up the right to receive future monthly benefit payments in exchange for a cash-out payment now—typically, the actuarial net present value of your age-65 benefit, discounted to today. Taking the money up front gives you flexibility.