Unlike a traditional 401(k) plan, SEP IRAs have little to no administrative overhead. Companies with only a single employee can take advantage of SEP IRAs, meaning they can be a good choice for solo entrepreneurs or gig workers. Most importantly, SEP IRAs offer more generous tax breaks than personal IRAs.

Is SEP IRA better than 401k?

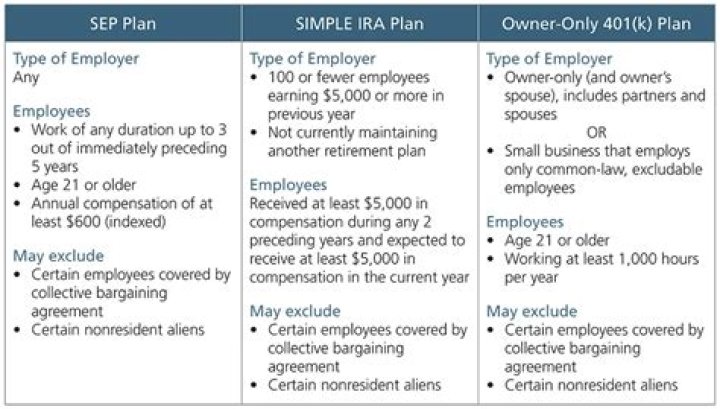

Owners of small businesses have more choices today when it comes to saving for retirement. Those who have full-time employees can save for retirement using a SEP IRA, while solo practitioners can choose between that and a solo 401(k) plan that has higher contribution limits and other advantages.

Can you max out 401k and SEP IRA?

You can opt for both if you choose. Keep in mind that the contribution limit for the SEP IRA will be limited by the profit-sharing contribution in the 401(k). They cannot combine to be more than 25% of total compensation. There’s no double-dipping, so there’s little value in establishing both retirement plans.

Can A S Corp have both of the 401K account and Sep account?

My California S-Corp has a 401K plan available to all employees. And a SEP plan that our owner and 2 other employees qualify for. We are already in compliance for our 401K for 2010, and are looking in … read more

Can a SEP IRA be used for a corporation?

A SEP IRA for S Corp is a type of pension plan that you may be able to set up for your corporation’s employee. There are many types of retirement plans that employers can choose for their employees, including a Simplified Employer Pension (SEP). SEP-IRAs cannot be used by individuals who are not a part of a business.

Can a SEP contribution be made from a personal account?

I suspect that making the SEP contribution from a personal account would not affect liability protection of the LLC since doing so would serve to not reduce the assets in the business account that would available to cover liability claims. June 3, 2019 4:44 PM

How does a simplified employee pension ( SEP ) plan work?

A Simplified Employee Pension (SEP) plan provides business owners with a simplified method to contribute toward their employees’ retirement as well as their own retirement savings. Contributions are made to an Individual Retirement Account or Annuity (IRA) set up for each plan participant (a SEP-IRA).