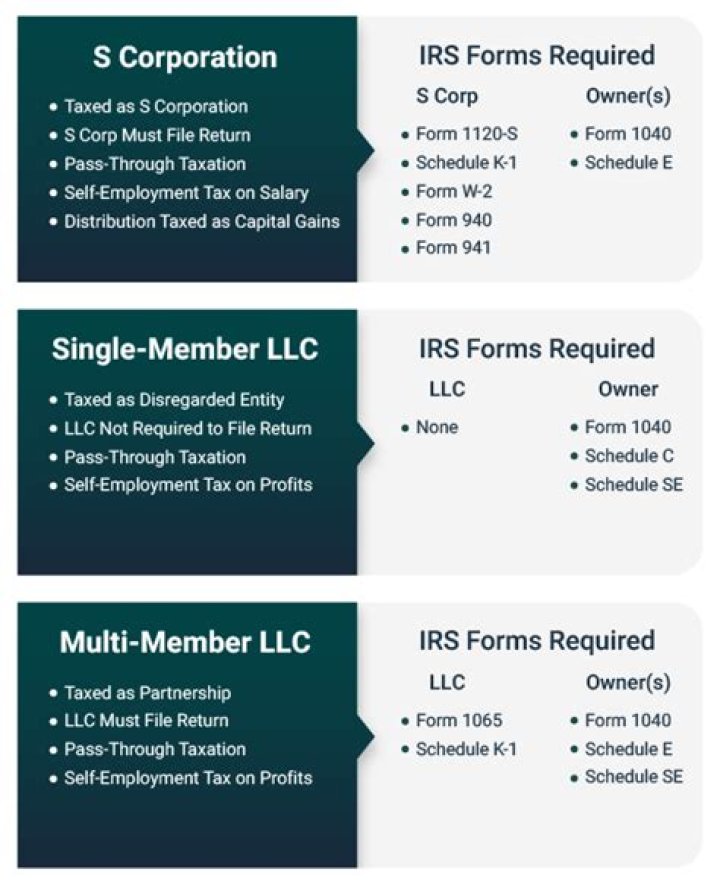

The big benefit of S-corp taxation is that S-corporation shareholders do not have to pay self-employment tax on their share of the business’s profits. The big catch is that before there can be any profits, each owner who also works as an employee must be paid a “reasonable” amount of compensation (e.g., salary).

Can I have a limited company and be self-employed?

Many of these also apply if you own a limited company but you’re not classed as self-employed by HMRC. Instead you’re both an owner and employee of your company. You can be both employed and self-employed at the same time, for example if you work for an employer during the day and run your own business in the evenings.

Are S Corp earnings subject to self-employment?

S-Corp distributions If you organize your business as an S-corporation, you can classify some of your income as salary and some as a distribution. You’ll still be liable for self-employment taxes on the salary portion of your income, but you’ll just pay ordinary income tax on the distribution portion.

Is the owner of a s Corporation a self employed person?

Owners of S corporations are not self-employed, because they don’t pay self-employment tax (Social Security and Medicare tax) on their distributions from the business.

Can a multiple owner LLC be considered self employed?

The owners of a multiple-owner LLC run their business in the same way as partners in a partnership. S corporation owners are not considered self-employed in the same way as partners in a partnership. They do not have to pay self-employment tax on their share of the corporation’s income.

Who is considered to be self employed by the IRS?

Here’s why: The IRS defines someone as being self-employed if they: This definition of being self-employed also includes owners of a limited liability company (LLC), because they are taxed as sole proprietors (single-member LLC) or partners (multiple-member LLC). Shareholders of corporations are not considered self-employed.

What does it mean to be self employed in a partnership?

S corporation owners are considered self-employed in the same way as partners in a partnership. S corporation owners receive a distributive share of the company’s income, just as partners in a partnership. If the S corporation owner also works in the business as an employee, they are paid a salary for that work.