Expensing a cost indicates it is included on the income statement and subtracted from revenue to determine profit. Capitalizing indicates that the cost has been determined to be a capital expenditure and is accounted for on the balance sheet as an asset, with only the depreciation showing up on the income statement.

What are non capitalized costs?

Non-Capital Cost. The costs necessary to carry, operate, and maintain the functionality and appearance of an asset over its service life after its installation.

What assets are not capitalized?

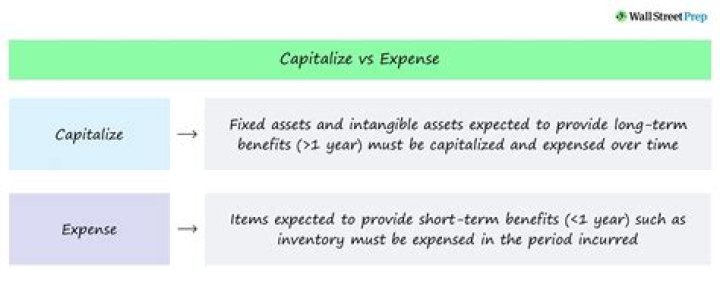

Typically, an item is not considered to be an asset to be capitalized unless it has a useful life of at least one year. Additionally, fixed assets are generally thought be items that are new or replacement in nature, rather than for the repair of an item.

What is a capitalized expense?

A capitalized cost is an expense that is added to the cost basis of a fixed asset on a company’s balance sheet. Capitalized costs are not expensed in the period they were incurred but recognized over a period of time via depreciation or amortization.

Unlike capitalizing a purchase, when you expense it, the expense directly reduces the company’s net income. In addition to routine operating costs such as payroll, auto expenses, bank charges, etc., there are other items that are always expensed versus capitalized.

What is improper capitalization?

Improper Capitalization of Costs. ONE OF THE MOST common methods of fraudulently making a company appear financially stronger is through the capitalization or deferral of expenses. This method instantly takes expenses, which reduce net income, and converts them into assets.

What happens when you capitalize an expense?

To capitalize is to record a cost or expense on the balance sheet for the purposes of delaying full recognition of the expense. In general, capitalizing expenses is beneficial as companies acquiring new assets with long-term lifespans can amortize or depreciate the costs. This process is known as capitalization.

Can you capitalize repairs and maintenance?

Repairs and maintenance are expenses a business incurs to restore an asset to a previous operating condition or to keep an asset in its current operating condition. This type of expenditure, regardless of cost, should be expensed and should not be capitalized.

When is a capitalized cost recognized as an expense?

November 27, 2017/. A capitalized cost is recognized as part of a fixed asset, rather than being charged to expense in the period incurred.

Why are transport costs included in capitalized costs?

Transport costs incurred to bring a purchased asset to its intended location Testing costs incurred to ensure that an asset is ready for its intended use Capitalization meets with the requirements of the matching principle, where you recognize expenses at the same time you recognize the revenues that those expenses helped to generate.

What is the matching principle for capitalized costs?

Understanding Capitalized Costs. When capitalizing costs, a company is following the matching principle of accounting. The matching principle seeks to record expenses in the same period as the related revenues.

Can a company capitalize more than it needs to?

Capitalizing too much. Make sure the company does not capitalize more than it needs to. E.g. you wouldn’t want to see a company capitalized 100% of its R&D cost. Be wary of software development costs being capitalized. Early stage research and development should be expensed while later stage developments can be capitalized.